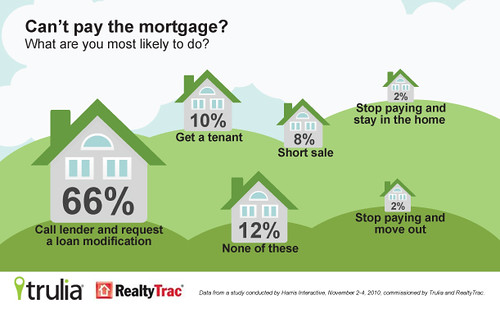

Short sales are all the rage in the USA these days.

And, that’s not something to celebrate.

Why?

Because if people are “short selling”, times are not good. The short sale has become one of the most popular “tools of choice” since the global financial crisis hit the world like a tsunami in 2008.

So, just what is a short sale?

What is it?

Basically, a short sale is when the bank agrees to let a homeowner sell a home for less than what’s owed on the mortgage.

Why would a bank do that?

Why would an owner do that?

What’s in it for the bank?

The bank would do a short sale deal to get the asset off the books.

Did you ask, “What asset?”

Good question, because it’s not the asset you think.

For the bank, the asset is the mortgage holder. And, in a short sale situation, the bank wants to get rid of the asset – the mortgage holder.

Why?

Because the mortgage holder isn’t paying the mortgage for some reason. And, the bank sees no way to get the mortgage holder to keep paying.

Normally, in a short sale situation, the mortgage holder is sunk. There’s no money to pay. Either the person has lost their job and can’t pay or, for an investment property, there’s not enough rent coming in. Either way, the mortgage is not getting paid and the bank is essentially powerless to change this situation. Better to get rid of the asset – the non-paying mortgagee.

What’s in it for the troubled home owner?

Why would a homeowner agree to – or ask for – a short sale. Well, let’s take a real life example. I’ve already bought one short sale home and I’m in the process of buying another one. I’ve asked my real estate agent the same question, “Why are they doing a short sale?”

Here’s what she told me.

The owner is from California and came over here (Florida) in the boom and bought 5 or 6 houses. He was told they would rent for $1,400 a month.

He never talked to a local agent because we would have told him, we’ve never seen rents like that. The most would have been about $900 a month. The people selling the properties kept their customers away from anyone local. And, it worked. We had lots of people coming in from California buying up everything at high prices.

So, now he’s got 5 or 6 properties, all worth less than half what he paid for them and only pulling in about $700 a month in rent each. He’s not only underwater, but it’s costing him over $3,000 a month to hold these properties.

A short sale will get him out of this situation. A short sale looks really good compared to his current situation.

This is a classic example of someone opting for a short sale.

Did you say penalties?

Now the short sale does come with some penalties over and above the initial losses. As I understand it, the federal government treats the unpaid loan balance as income. As such, they want to tax it. And, this can be quite substantial.

Let’s take our investor above. Let’s say he’s got 5 properties and paid $200,000 each. Now if the bank agrees to a short sale of only $100,000 each, he’s looking at a tax bill on half a million bucks!

Crushing.

I’m not sure I agree with this arrangement, because a short sale is a business agreement between the bank and the homeowner. If the bank wants to write off the loan, why can’t they? If the bank wants to give you a deal (get rid of you as an asset), why can’t they?

All that’s happened here is this … the bank has agreed to wipe out the loan following the sale of the property. That’s not income to the home owner. That’s just the bank saying, “You don’t have to pay us back. Our deal is over.”

So, where’s the income?

I don’t understand how the federal government – in good conscience – can step into this private deal and tax the homeowner for income never received. It’s seems, well … unfair, harsh, cruel, wrong … pick a word …

Short sale … now a common word in the real estate vocabulary.

I wish it wasn’t.